STAINLESS STEEL TRADING MARKET OUTLOOK 2026: GLOBAL SUPPLY SHIFTS AND INDIA'S DEMAND ENGINE

Global stainless steel output is set to expand for a fourth consecutive year in 2026, but the growth math is increasingly lopsided: Asia adds tonnes while Europe contracts, Indonesia keeps cost floors low, and trade defence walls rise across nearly every major importing region. For Indian traders and mills, the backdrop is a domestic demand cycle running at 7-9% against a rapidly reshaping tariff map in the EU, US, and at home. The themes below track what the data show heading into the rest of calendar 2026 and FY27.

A SLOWER BUT STILL-EXPANDING GLOBAL MELT BOOK

Worldstainless reported global crude stainless steel production at 64.16 million tonnes in 2025, up 2.1% year-on-year, a sharp deceleration from the 7% print in 2024. Q4 2025 grew just 0.8%, reflecting weak Chinese mill margins and a second consecutive year of EU melt-shop decline. Analyst consensus (SMM, Fastmarkets, Mordor) pegs 2026 global growth at 2-3%, taking output toward 65.5-66.0 Mt. China alone represented 63.7% of world production in 2025 at 40.87 Mt, and the Asia-ex-China basket (Indonesia, India, South Korea, Japan, Taiwan) added another 14.4 Mt.

Capacity additions remain concentrated in the Indonesia-India corridor. In Morowali, the PT Glory Metal Indonesia JV between Tsingshan and Jindal Stainless commissioned its 1.2 Mt/yr melt shop in March 2026, ahead of schedule. The POSCO-Tsingshan Xinheng JV (2.0 Mt/yr, USD 708 million) broke ground in October 2025, with construction running through 2026. Combined with Delong’s Dexin expansions, Indonesian stainless capacity is tracking from ~7.5 Mt in 2024 to roughly 9 Mt by 2027. In India, installed primary stainless capacity sits near 7.5 Mt, with Jindal Stainless Ltd, the country’s largest producer, reaching 4.2 Mt consolidated melt capacity after the Indonesia JV commissioning.

Europe is moving the other way. Outokumpu’s European EBITDA swung to a loss of EUR 46 million in 2025, and the company has placed a EUR 200 million Tornio annealing/pickling investment under review while studying partial closures at Krefeld. Aperam’s stainless and electrical steel operating income fell to EUR 19 million from EUR 75 million, and its Genk plant faced a potential shutdown in late October 2025 on energy costs.

Table 1. Global crude stainless steel production by region (kt)

Source: worldstainless (Feb 2026); 2026f based on analyst consensus (SMM, Fastmarkets, Mordor Intelligence).

End-use demand continues to tilt toward building and construction, which market-research sources place at ~36% of 2025 volume, followed by metal goods and appliances, mechanical engineering, and automotive. Mordor flags automotive at a 5.3% volume CAGR (battery enclosures, fuel-cell stacks) and duplex grades at 5.3% CAGR on electrolyzer orders.

NICKEL SURPLUS ANCHORS PRICES; FERROALLOYS DIVERGE

LME three-month nickel traded at USD 17,171/t on 1 April 2026, within a USD 16,500-18,500/t band since January. LME stocks climbed to 287,550 tonnes in March, the highest in over four years and +44% year-on-year. INSG and Argus project a 2026 refined nickel surplus of 261-288 kt, driven by Indonesian MHP capacity almost doubling to 862 kt/yr of contained nickel by 2026. Consensus 2026 price forecasts span a wide range: ING USD 15,250/t average, Goldman Sachs USD 17,200/t, Fastmarkets and Wood Mackenzie USD 17,000-19,000/t. The swing factor is Indonesia’s 2026 ore quota, set at 260-270 Mt versus 379 Mt in 2025, and whether enforcement holds.

Ferrochrome tells a different story. High-carbon 50% Cr traded around CNY 8,400-8,550/t in Inner Mongolia in April 2026 and US prices firmed 1.4% QoQ to USD 3,737/t in Q1, supported by South African power cuts and Glencore’s Lion smelter restart. Molybdenum oxide jumped to USD 23.43/lb in January 2026 (+9.3% MoM) and spiked to USD 36/lb in the US after the Langeloth facility fire, with SMM forecasting a 13,000-tonne deficit in 2026. Net effect: 300-series cost floors stay soft on nickel, while 400-series and moly-bearing grades (316/duplex) face a modest bullish bias.

Base prices for 304 cold-rolled coil are holding range-bound. CRU (November 2025) flagged prices range-bound through Q1 2026, with excess capacity capping upside and raw-material floors protecting downside. Asian 304 CR export offers sat at USD 3,200-3,400/t in late 2025, European ex-works at EUR 3,450-3,700/kg including surcharges, and Indian 304 CRC at roughly INR 180/kg in Mumbai in February 2026.

TRADE WALLS ARE RISING ON ALMOST EVERY COAST

The trade-policy map has thickened materially. The US Section 232 steel tariff doubled to 50% in June 2025 (UK at 25%), and a 2 April 2026 proclamation restructured the duty to apply to the full customs value of finished and derivative goods, effective 6 April 2026. The EU’s CBAM definitive phase began on 1 January 2026, with certificate surrender starting February 2027 and stainless steel fully in scope. A 17 December 2025 Commission proposal would extend CBAM to roughly 180 downstream products from 2028.

The EU also agreed provisionally on 13 April 2026 to replace the current steel safeguard from 1 July 2026 with tariff-rate quotas cut by about 47% to 18.3 Mt/yr, an out-of-quota duty of 50% (up from 25%), and a mandatory ‘melted and poured’ origin rule from 1 October 2026. MEPS and Damstahl estimate the stainless duty-free quota will shrink by roughly 54% versus today. Definitive EU anti-dumping and countervailing duties on Indonesian cold-rolled stainless (AD 19.3%, CVD 20.5%) were extended to Taiwan, Turkey, and Vietnam via the anti-circumvention Regulation 2024/1267.

China imposed 23-103% AD on stainless billets and HR from South Korea, the EU, UK, and Indonesia from 1 July 2025. Chinese stainless exports fell 0.3% to 5.03 Mt in 2025 and imports from Indonesia dropped 21.6% to 1.23 Mt. Export-licensing measures under MOFCOM/GACC Announcement No. 79 took effect on 1 January 2026, though CRU expects limited direct stainless impact. Red Sea routing remains unstable; most Asia-Europe carriers continue via the Cape, keeping Asia-Europe spot freight 25-40% above pre-crisis levels per Xeneta.

INDIA: DEMAND MOMENTUM MEETS AN IMPORT PILE-UP

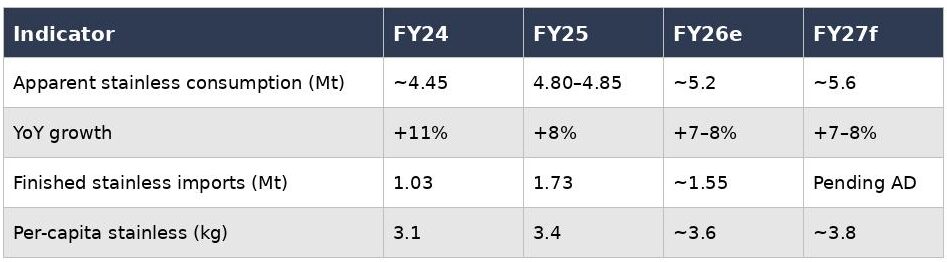

India’s stainless steel apparent consumption rose about 8% to 4.80-4.85 Mt in FY25, per ISSDA, with the association guiding 7-8% growth over FY26-FY28 on infrastructure capex, railways (Vande Bharat and metro coaches), automotive, ornamental pipes and tubes, lifts and elevators, and kitchenware. Per-capita stainless consumption sits at 3.4 kg against a global average near 6 kg, giving long headroom. JSL’s Q3 FY26 volumes rose 11% year-on-year to 650 kt, and 9M FY26 consolidated PAT grew 23%.

Imports remain the sector’s core irritant. Finished stainless imports hit 1.73 Mt in FY25, with China, Indonesia, Vietnam, and South Korea as top origins. Data for the first five months of FY26 show total steel imports down 14% under the broader safeguard, while stainless-specific flats fell roughly 15%. Chinese volumes halved, but Vietnam rose 72% year-on-year, reinforcing circumvention concerns raised by ISSDA.

Table 2. India stainless steel demand and import indicators

Sources: ISSDA, BigMint, IBEF, JSL investor presentations.

On trade remedies, the DGTR initiated an anti-dumping investigation on 29 September 2025 into cold-rolled stainless flats (300 and 400 series) from China, Indonesia, and Vietnam, on a petition led by ISSDA and Jindal Stainless. A definitive 11.5% steel safeguard runs from 21 April 2026 through April 2027 on carbon and alloy flats, but explicitly excludes stainless, CRGO, and coated products. The Cookware and Utensils QCO covering stainless utensils (IS 14756:2024) and sinks (IS 13983:1994) took effect on 1 October 2025 for large units, with micro units onboarded by April 2026, though a 2026 revision is reportedly narrowing the scope. The Ministry of Steel launched PLI 1.2 in November 2025 with 4-15% incentives on incremental sales of specialty steel across FY26-FY30, and the Green Steel Taxonomy (December 2024) now covers 25 certified mills.

THE PRODUCER LANDSCAPE IS CONSOLIDATING AROUND FEWER, BIGGER NAMES

India has roughly 7.5 Mt of installed primary stainless capacity running at about 60% utilisation. JSL, India’s largest stainless producer, consolidated at 4.2 Mt (3.0 Mt India + 1.2 Mt Indonesia JV from March 2026), targets 3.5 Mt sales by FY29, and has signed a non-binding MoU with Maharashtra for a phased 4 Mt greenfield plant (INR 40,000 crore over 10 years). Viraj Profiles (0.53 Mt long products, largely export), SAIL Salem (0.18 Mt melt), Mukand, MIDHANI for specialty and defence grades, and Panchmahal Steel round out the primary set. Shah Alloys flagged going-concern uncertainty in February 2026 after an August 2025 plant shutdown.

Backward integration is deepening. JSL’s 49% stake in the New Yaking NPI smelter in Halmahera (200 kt/yr, commissioned August 2024) supplies roughly 16% of its nickel needs, while captive ferrochrome (250 kt/yr at Jajpur) keeps alloy costs hedged. FY26 ferrous scrap imports rose 45% to 5.7 Mt through October 2025, with stainless-specific scrap imports more than doubling to 1.06 Mt, underscoring India’s continued reliance on imported scrap (roughly 75% of stainless scrap needs) and persistent nickel import dependence.

WHAT TO WATCH IN 2026

Four forward indicators will shape how the year resolves. First, Indonesian nickel ore quota compliance: any slippage above the 270 Mt 2026 cap would push LME nickel back through USD 17,000/t and reflate 300-series surcharges within 4-8 weeks. Second, DGTR’s preliminary findings on the CR stainless flats case against China, Indonesia, and Vietnam, which could reset India’s import mix for H2 FY27. Third, the implementation detail of EU CBAM default emissions values and the mid-2026 safeguard adoption, which together will determine landed-cost economics for Asian slab and coil into Europe. Fourth, the pace of new Indonesian and Indian capacity commissioning, particularly whether POSCO-Tsingshan Xinheng advances on schedule and whether JSL’s Jajpur HRAP and cold-rolling expansions land in Q2-Q4 FY27 as guided.

The direction of travel is clear: more tonnes from fewer origins, tighter borders, and a domestic Indian market that is increasingly the demand engine the rest of the industry is watching.

ABOUT JSLGC

Singapore-based JSL Global is one of the fastest-growing privately held companies operating in the global stainless steel ecosystem. In just five years, we’ve become a trusted and preferred partner for businesses across the value chain, with reliable metal and mineral sourcing facilities, a strong global trading network of stainless steel products, strategic investments in RKEF plants, and 1 GW RTC clean power projects under implementation.

Operating to the highest ESG standards globally, we are committed to achieving net-zero carbon emissions by 2050.

MEDIA ENQUIRIES

Topendra Nayak: investments@jslgc.com